Are you heading to Greenville, SC, this summer? Use this guide to figure out what to do in Greenville, SC this summer for a fun trip.

Read More >>

If you are a first-time borrower, read this guide to learn about our title loan basics. Once you understand, fill out the online form!

Read More >>

Considering a signature installment loan? Discover how they work and when to use them in this helpful article!

Read More >>

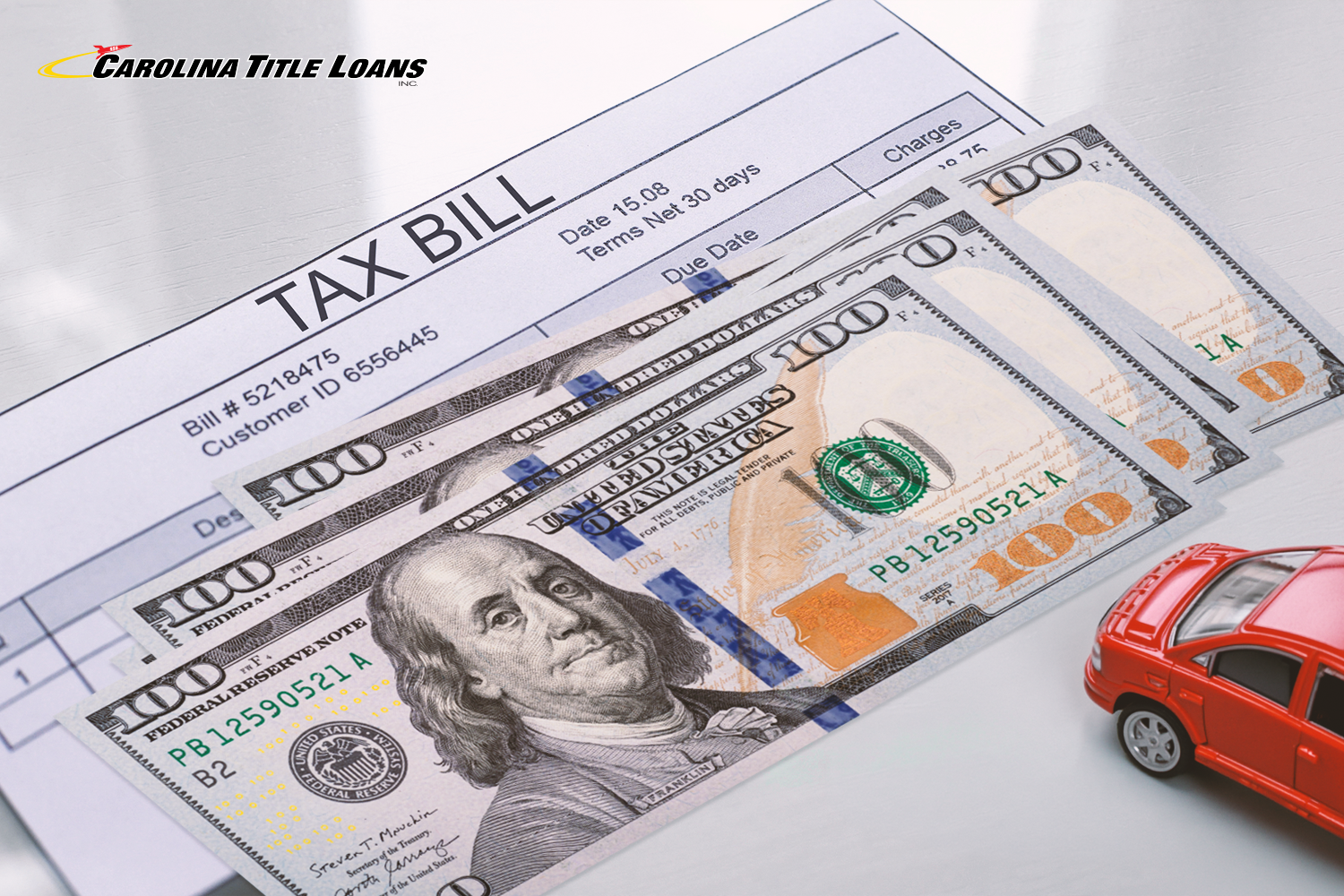

Learn seven ways to help handle an emergency tax bill. Discover tax bill loans in SC that can help, such as title loans.

Read More >>

Do you need emergency cash but have bad credit? Learn how to get bad credit title loans in SC to fund urgent costs!

Read More >>

Need help affording emergency appliance repair in SC? Learn how to pay for repairs to your oven, microwave, washing machine, etc., with title loans in South Carolina!

Read More >>

Do you need fast emergency cash? Learn how to leverage your vehicle's value without losing it with a title loan in South Carolina!

Read More >>

Have you been laid off in South Carolina? Find out how to handle expenses after getting laid off and affording rising utility bill costs.

Read More >>

Need a title loan but don't have a job? Learn how to get a title loan while unemployed with Carolina Title Loans, Inc. Borrow up to $15,000 today!

Read More >>

Do you work part-time but need fast cash for an emergency? Learn how to get a title loan if you work part-time!

Read More >>